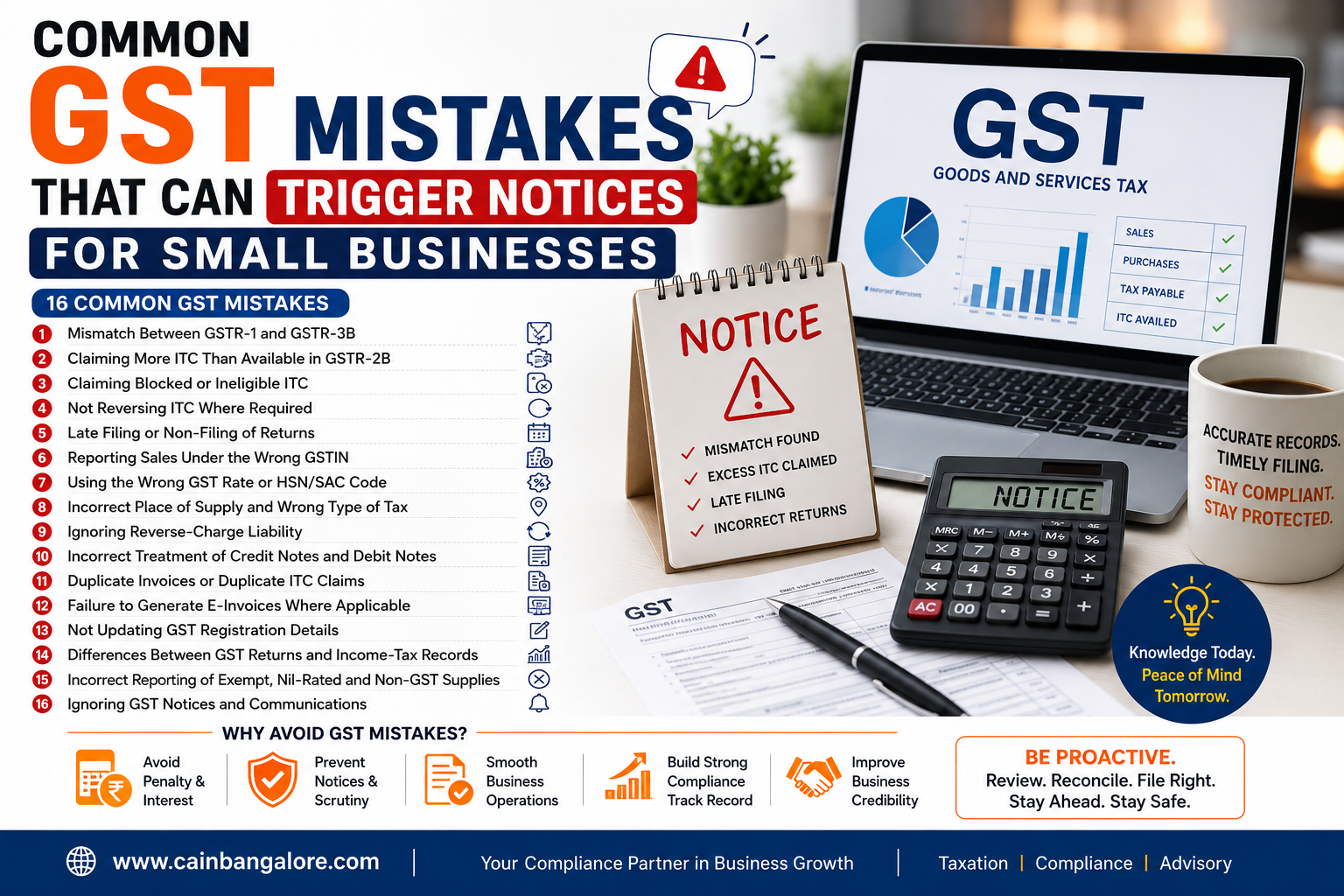

Common GST Mistakes That Can Trigger Notices for Small Businesses

GST compliance is not limited to filing returns before the due date. The information reported in sales invoices, purchase records, e-invoices, GSTR-1, GSTR-3B and GSTR-2B must also remain consistent.

The GST system increasingly uses automated comparisons to identify mismatches. Even a genuine accounting error can result in an intimation, scrutiny notice, demand for explanation, restriction on return filing or, in serious cases, cancellation proceedings.

Small businesses are particularly vulnerable because bookkeeping, invoicing and return filing may be handled by different people. A mismatch between the accountant’s records, the GST portal and the returns filed can easily go unnoticed.

Here are the most common GST mistakes that can trigger notices and the steps businesses can take to avoid them.

1. Mismatch Between GSTR-1 and GSTR-3B

GSTR-1 contains invoice-wise details of outward supplies, while GSTR-3B contains the summary of tax liability and input tax credit.

A notice or system-generated intimation may arise when the taxable turnover or tax liability reported in GSTR-1 is higher than the liability discharged through GSTR-3B.

For example, a business may report sales of ₹10 lakh in GSTR-1 but pay GST on only ₹8 lakh in GSTR-3B. The portal may treat the difference as unpaid tax unless it is properly explained.

Where the difference exceeds the system-defined threshold, the taxpayer may receive an intimation in Form GST DRC-01B. The taxpayer must provide the reason for the difference or pay the differential liability. Failure to submit the required response may also affect the filing of GSTR-1 or IFF for a subsequent period.

Common reasons for this mismatch

- Sales invoices omitted from GSTR-3B

- Credit notes entered in one return but not the other

- Wrong tax period selected

- Amendments reported incorrectly

- Advances or reverse-charge transactions wrongly classified

- Interstate sales reported as intrastate sales

- Manual data-entry mistakes

How to avoid it

Before filing GSTR-3B, reconcile:

- Taxable turnover in the sales register

- Liability reported in GSTR-1

- Liability appearing in the GSTR-3B system-generated summary

- Debit notes and credit notes

- Amendments relating to previous periods

Do not file GSTR-1 and GSTR-3B independently without completing a return-to-return reconciliation.

2. Claiming More Input Tax Credit Than Available in GSTR-2B

GSTR-2B is an auto-drafted input tax credit statement generated from the information reported by suppliers.

A common mistake is claiming input tax credit in GSTR-3B merely because the business possesses a purchase invoice, without checking whether the invoice appears in GSTR-2B.

When the ITC claimed in GSTR-3B exceeds the eligible credit reflected in GSTR-2B beyond the prescribed system limit, the taxpayer may receive an intimation in Form GST DRC-01C. The taxpayer must reconcile the difference and submit a response in Part B of the form.

Possession of an invoice alone may not be sufficient. Input tax credit is subject to the eligibility conditions prescribed under Section 16 of the CGST Act and the documentary requirements under Rule 36.

Common causes of excess ITC claims

- Supplier has not filed GSTR-1

- Supplier reported an incorrect GSTIN

- Invoice has been uploaded in a later tax period

- Credit note has not been considered

- Same invoice has been claimed twice

- Ineligible personal expenses have been included

- Blocked credits have been claimed

- Import or reverse-charge credit has been reported incorrectly

How to avoid it

Prepare a monthly reconciliation between:

- Purchase register

- GSTR-2B

- ITC claimed in GSTR-3B

- Ineligible ITC

- ITC requiring temporary reversal

- ITC eligible for reclaim in later periods

Follow up with suppliers immediately when invoices do not appear in GSTR-2B.

3. Claiming Blocked or Ineligible Input Tax Credit

Not every GST amount paid on a business expense is eligible for input tax credit.

Certain categories of credit are restricted or blocked under Section 17(5) of the CGST Act. Depending on the facts and statutory exceptions, restrictions may apply to expenses relating to motor vehicles, food and beverages, club membership, personal consumption, employee-related benefits, construction of immovable property and goods that are lost, stolen, destroyed, written off or given away as gifts or free samples.

Common examples

- ITC claimed on a car used by the proprietor

- GST credit on restaurant bills

- ITC on personal travel expenses

- Credit on gifts distributed to customers

- ITC on construction or renovation of an office building

- Credit on invoices issued in an employee’s name

- ITC on goods used partly for exempt supplies

How to avoid it

Classify expenses before claiming credit. Maintain separate ledger accounts for:

- Eligible ITC

- Blocked ITC

- Common ITC

- Personal expenses

- Exempt-supply-related expenses

- Capital goods

Where inputs or capital goods are used for both taxable and exempt activities, the relevant reversal provisions may apply.

4. Not Reversing ITC Where Required

Input tax credit may initially appear eligible but may later require reversal.

Examples include:

- Non-payment to a supplier within the prescribed period

- Goods or services used for exempt supplies

- Personal or non-business use

- Credit relating to supplier credit notes

- Invoices later found to be invalid

- Common inputs used for taxable and exempt activities

Businesses often claim the credit correctly at first but fail to track subsequent events that require reversal.

The GST return format requires taxpayers to report ITC availment, reversals and ineligible credit correctly in Table 4 of GSTR-3B.

How to avoid it

Maintain an ITC reversal register containing:

- Invoice number

- Supplier name

- Original ITC claimed

- Reason for reversal

- Date of reversal

- Amount reversed

- Date and eligibility of reclaim, where permitted

5. Filing GST Returns Late or Not Filing Them at All

A registered taxpayer must continue filing applicable GST returns even when there is no business activity.

Failure to file returns can lead to:

- Late fees

- Interest

- Notice to non-filers

- Blocking of subsequent returns

- Suspension or cancellation proceedings

- Difficulty in obtaining loans, tenders or vendor approvals

The CGST Rules provide for the issue of a notice in Form GSTR-3A to non-filers.

Even businesses dealing only in exempt goods must file returns while their GST registration remains active, unless they apply for cancellation where legally appropriate.

How to avoid it

Create a compliance calendar covering:

- GSTR-1

- GSTR-3B

- QRMP-related filings

- Composition returns

- Annual return

- E-invoice reporting

- TDS or TCS returns, where applicable

Nil returns should also be filed within the applicable timelines.

6. Reporting Sales Under the Wrong GSTIN

Businesses operating from multiple states may have separate GST registrations.

A common mistake is raising invoices under the wrong state GSTIN or reporting transactions in the return of a different registration.

For example, a Bengaluru branch may supply goods, but the invoice may be issued using the GSTIN of the Chennai office. This can create discrepancies relating to:

- Place of supply

- Tax payment

- Input tax credit of the customer

- Turnover reported by each registration

- Stock transfers between branches

How to avoid it

Configure billing software separately for every GSTIN. Each registration should have its own:

- Invoice series

- Sales register

- Purchase register

- E-invoice credentials

- E-way bill credentials

- Return reconciliation

7. Using the Wrong GST Rate or HSN/SAC Code

Applying an incorrect GST rate can lead to short payment of tax or excess collection from customers.

The error may arise because:

- The product was classified under the wrong HSN code

- A service was treated as goods

- An exempt supply was treated as taxable

- A concessional rate was applied without satisfying conditions

- The applicable rate changed but billing software was not updated

Possible consequences

If a lower rate is applied incorrectly, the department may demand:

- Differential tax

- Interest

- Penalty, depending on the circumstances

If excess GST is collected, the business cannot automatically treat it as additional income.

How to avoid it

Maintain an approved product-and-service tax master containing:

- Description

- HSN or SAC

- GST rate

- Exemption notification, if any

- Effective date of rate

- Supporting classification note

Review the tax master whenever rates or business activities change.

8. Incorrect Place of Supply and Wrong Type of Tax

The place-of-supply rules determine whether a transaction attracts:

- CGST and SGST, or

- IGST

Small businesses frequently charge CGST and SGST when IGST is applicable, or charge IGST where the supply is intrastate.

Common problem areas include:

- Services provided to customers in another state

- Installation services

- Events and training programmes

- Transportation

- Online services

- Property-related services

- Supplies made through e-commerce platforms

- Bill-to and ship-to transactions

How to avoid it

Verify the following before raising an invoice:

- Supplier’s location

- Customer’s GSTIN and state

- Delivery address

- Place where the service is performed

- Nature of the supply

- Applicable place-of-supply provision

Do not determine the tax type merely from the customer’s billing address.

9. Ignoring Reverse-Charge Liability

Under reverse charge, the recipient may be required to pay GST directly to the government.

Businesses sometimes ignore reverse-charge transactions because the supplier has not charged GST on the invoice.

Potential reverse-charge transactions may include specified legal services, director-related services, goods transport agency services and other notified supplies, subject to the applicable conditions.

Common errors

- RCM liability not reported

- RCM tax paid using ITC instead of cash

- ITC claimed without first paying the reverse-charge liability

- Supplier transaction wrongly treated as forward charge

- Self-invoice or payment voucher requirements ignored

How to avoid it

Create a separate reverse-charge ledger and review every month:

- Legal and professional expenses

- Director payments

- Transport expenses

- Imports of services

- Transactions with notified suppliers

10. Incorrect Treatment of Credit Notes and Debit Notes

Credit notes affect taxable turnover and tax liability. When they are not properly reflected in the books and GST returns, mismatches can arise between:

- GSTR-1

- GSTR-3B

- Customer records

- Supplier records

- Annual return

Common mistakes

- Credit note entered in accounting software but not in GSTR-1

- Commercial credit note wrongly treated as a GST credit note

- Wrong original invoice linked

- Incorrect taxable value or GST amount

- Credit note reported in the wrong financial year

- Customer has already reversed ITC, but supplier has not adjusted the output liability

How to avoid it

Maintain a credit-note register and link every GST credit note to:

- Original invoice

- Reason for issue

- Taxable value

- GST amount

- Return period

- Customer communication

11. Duplicate Invoices or Duplicate ITC Claims

Duplicate entries may occur when invoices are imported from multiple systems or entered manually more than once.

A duplicated sales invoice can increase turnover and tax liability. A duplicated purchase invoice can result in excess ITC and may trigger an ITC mismatch intimation.

How to avoid it

Use accounting controls that block duplicate combinations of:

- Supplier GSTIN

- Invoice number

- Invoice date

- Taxable value

- GST amount

Review unusual or repeated invoice numbers before filing returns.

12. Failure to Generate E-Invoices Where Applicable

Taxpayers covered by the e-invoicing mandate must generate an Invoice Reference Number and comply with the prescribed e-invoice process for applicable transactions.

The current notified applicability generally covers businesses whose aggregate turnover crossed ₹5 crore in any relevant financial year, subject to statutory exclusions and transaction-specific rules.

For businesses with annual aggregate turnover of ₹10 crore or more, e-invoices older than 30 days cannot be reported on the invoice-registration portal from 1 April 2025.

Common mistakes

- E-invoice not generated

- Invoice issued before generating IRN

- Wrong GSTIN reported

- Incorrect document type selected

- E-invoice cancelled after the permitted time

- QR code missing from the invoice

- E-invoice generated but accounting records not updated

- Old invoices uploaded after the allowed reporting window

How to avoid it

Check e-invoice applicability based on aggregate turnover from earlier financial years, not merely the current year’s turnover.

Integrate the billing system with the invoice-registration portal and monitor failed IRN requests daily.

13. Not Updating GST Registration Details

Businesses must keep their GST registration information current.

Notices may arise when:

- Principal place of business has changed

- Additional business location is not added

- Partners or directors have changed

- Bank account details are incorrect

- Email address and mobile number are inactive

- Nature of business has changed

- The business is not found at the registered address

The CGST Rules require prescribed changes in registration particulars to be submitted within the specified period.

How to avoid it

Review the GST registration certificate at least once every quarter and after every major business change.

Display the GST registration certificate and GSTIN at the business premises where required.

14. Differences Between GST Returns and Income-Tax Records

The turnover reported in GST returns may be compared with:

- Income-tax returns

- Tax audit reports

- TDS statements

- Annual Information Statement

- Bank receipts

- E-commerce data

- Financial statements

Not every difference is necessarily incorrect. GST turnover and accounting revenue can differ because of advances, stock transfers, exempt supplies, branch transactions, credit notes and other adjustments.

However, unexplained differences can attract scrutiny.

How to avoid it

Prepare an annual turnover reconciliation covering:

- Turnover as per financial statements

- Turnover as per GSTR-1

- Turnover as per GSTR-3B

- Exempt and zero-rated supplies

- Advances

- Credit notes

- Stock transfers

- Other income

- Non-GST income

Document the reason for every material difference.

15. Incorrect Reporting of Exempt, Nil-Rated and Non-GST Supplies

Businesses may wrongly assume that exempt sales need not be reported.

Incorrect or incomplete reporting of exempt, nil-rated and non-GST supplies can affect:

- Annual turnover

- ITC reversal

- Registration threshold calculations

- Annual return

- Financial-statement reconciliation

How to avoid it

Create separate accounting ledgers for:

- Taxable supplies

- Zero-rated supplies

- Exempt supplies

- Nil-rated supplies

- Non-GST supplies

- Out-of-scope transactions

16. Ignoring GST Portal Notices and Communications

Some businesses notice an email or SMS but fail to check the actual notice on the GST portal.

GST communications may appear under the “View Notices and Orders” section of the portal.

Ignoring a notice can result in:

- Ex parte order

- Confirmation of demand

- Penalty

- Recovery proceedings

- Blocking of return filing

- Registration suspension or cancellation

Registration cannot ordinarily be cancelled by the proper officer without issuing a show-cause notice and giving the taxpayer an opportunity to respond.

How to avoid it

Check the GST portal regularly rather than relying only on email alerts.

Maintain a notice register with:

- Date received

- Notice form

- Tax period

- Reply due date

- Person responsible

- Documents required

- Date of reply

- Current status

What Should You Do After Receiving a GST Notice?

Do not ignore the notice or immediately make payment without understanding the issue.

Step 1: Identify the form and reason

Determine whether it is:

- A return mismatch intimation

- A scrutiny notice

- A non-filer notice

- A registration notice

- A demand or recovery notice

- An e-invoice or e-way bill matter

Form GST ASMT-10 is used to communicate discrepancies identified during scrutiny of returns, while Form GST ASMT-11 is used by the taxpayer to submit a response.

Step 2: Check the deadline

Note the response due date immediately. Late replies can weaken the taxpayer’s position.

Step 3: Reconcile the figures

Compare:

- Books of account

- Filed returns

- GSTR-1

- GSTR-3B

- GSTR-2B

- E-invoice data

- E-way bill data

- Electronic cash and credit ledgers

Step 4: Prepare supporting documents

Depending on the issue, documents may include:

- Tax invoices

- Purchase invoices

- Credit notes

- Debit notes

- Bank statements

- Agreements

- Delivery challans

- E-way bills

- Payment proofs

- Supplier confirmations

- Reconciliation statements

Step 5: Pay only verified liability

Where a genuine short payment is identified, voluntary payment may be made through Form GST DRC-03 in eligible circumstances.

Step 6: Submit a clear reply

The reply should address every allegation separately and contain:

- Facts

- Reconciliation

- Legal position

- Supporting evidence

- Payment details, where applicable

- Request for closure of proceedings

Monthly GST Compliance Checklist for Small Businesses

Before filing GST returns, confirm that:

- All sales invoices are recorded

- Credit notes and debit notes are updated

- GSTR-1 agrees with the sales register

- GSTR-3B liability agrees with GSTR-1

- Purchase register is reconciled with GSTR-2B

- Ineligible ITC is excluded

- Required ITC reversals are completed

- Reverse-charge transactions are identified

- Correct GST rates and HSN/SAC codes are used

- Interstate and intrastate supplies are classified correctly

- E-invoices and e-way bills are reconciled

- GST payments are made from the correct ledger

- GST notices and portal communications are reviewed

- Supporting documents are securely maintained

Conclusion

Most GST notices received by small businesses are not caused by fraud. They are often triggered by mismatches, missed filings, incorrect ITC claims, wrong tax classifications or poor reconciliation.

The best defence against a GST notice is a disciplined monthly compliance process.

Businesses should not wait until the end of the financial year to reconcile their records. Monthly checks between the books of account, GSTR-1, GSTR-3B, GSTR-2B, e-invoice data and tax ledgers can identify errors before they become notices, interest liabilities or penalties.

Small mistakes can create major compliance problems. Accurate records, timely filing and regular reconciliation remain the most effective ways to reduce GST risk.

Disclaimer: This article is intended for general informational purposes only. GST applicability and legal consequences depend on the facts of each case and the law in force on the relevant date. Businesses should obtain professional advice before taking action on a GST notice or disputed tax position.