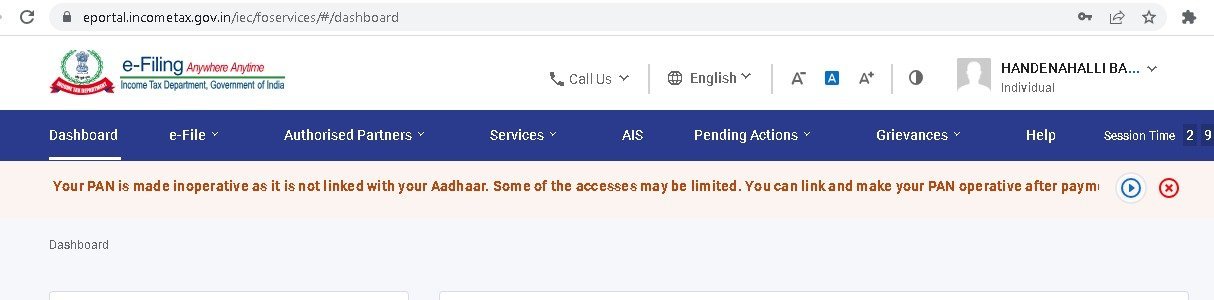

Where ITR data is electronically transmitted but e-verified or ITR-V (i) submitted beyond the time-limit of 30 days of transmission of data -in such cases the date of e-verification/ITR-V submission shall be treated as the date of furnishing the return of income and all consequences of late filing of return under the Act shall follow

CBDT Reduces tme limit for verification of ITR from 120 days to 30 days of transmitting the data of ITR electronically.